These days, many prospective homebuyers seem to be holding their breath wondering when interest rates will come down and waiting to make their move.

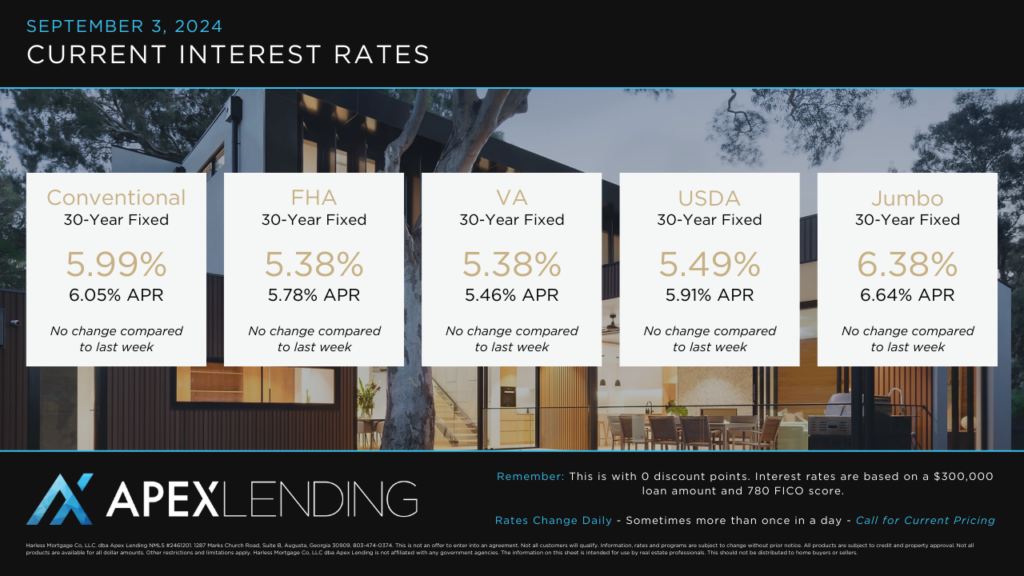

Here’s the latest from one of our preferred local lending partners, Jared Harless, with Apex Lending. Don’t hesitate to reach out to one of The Legacy Group SC Real Estate Team Members to discuss whether waiting to buy your next home or buying now would be a better option. The answer might surprise you!

Last week ended with stocks higher and mortgage bonds trading near unchanged levels after the Federal Reserve’s favorite measure of inflation, Personal Consumption Expenditures (PCE), showed mild month over month inflation. Let’s review the highlights and how this will impact rates moving forward.

Personal Consumption Expenditures

Personal Consumption Expenditures (PCE) showed that Headline (or all-in) inflation rose 0.155% in July, which was slightly below the expectations of 0.2%. Year over year inflation remained at 2.5% which was slightly better than the expected 2.6%.

The core rate, which strips out food and energy costs and is the main focus of the Federal Reserve, rose 0.161%. This was also slightly below the expectations of 0.2%. Year over year, core inflation remained at 2.62%.

The monthly core reading was very strong at 0.161%, and when annualized, is under the Federal Reserve’s 2% target at 1.93%. The previous three monthly readings were also very tame, and when annualizing the previous three month pace, it’s under the Federal Reserve’s target at 1.7%.

Inflation Pace Coming Within the Federal Reserve’s Target

Inflation is moderating and is moving to the Federal Reserve’s target. Despite good monthly progress, year over year progress has been difficult because of the low replacement values from last year. Looking at the components, shelter is still the largest contributor to the inflation readings, however, the lag in reporting is keeping Core PCE artificially high. Shelter rose 0.39% in July and contributed 0.07% to the monthly reading of 0.161%, which was 43% of the rise. Year over year shelter is up 5.27% within this report, and it’s contributing 0.93%, which is 35% of the total. Using real-time readings around 3% shows that Core PCE is being overstated by 0.4%, and when caught up, Core PCE would be at 2.22%

The other component that added about 26% in the monthly reading was Financial Services. Looking at all of the components, many were negative. Overall, a lot of the components are moderating or near the flatline, especially the goods sector.

Consumer spending rose 0.5%, which was also in line with estimates. Consumers continue to spend more than they take in, which is causing the savings rate to fall significantly. The savings rate was around 8% pre-pandemic, was cut in half to 4% in January of this year, but has since plummeted to 2.9% in July. This shows that consumers are under duress and there is only so much savings that consumers have to deplete. This should eventually lead to lower spending and a slowdown in the economy.

Bottom Line: Inflation is moderating and is moving in the right direction. With how inflation is annualized, year over year progress has been difficult and will remain difficult in Q4. Moving into Q1 of 2025, year over year inflation progress should be easier and move much closer to the Federal Reserve’s 2% goal. If we hit the 2% threshold, it should motivate the Federal Reserve to move more aggressively with rate cuts in 2025.

To begin working on a financial plan for your next mortgage, you can contact Jared at 803-474-0374 or [email protected]

Recent Comments